Food

California ‘billionaire tax’ makes ballot despite opposition from tech moguls

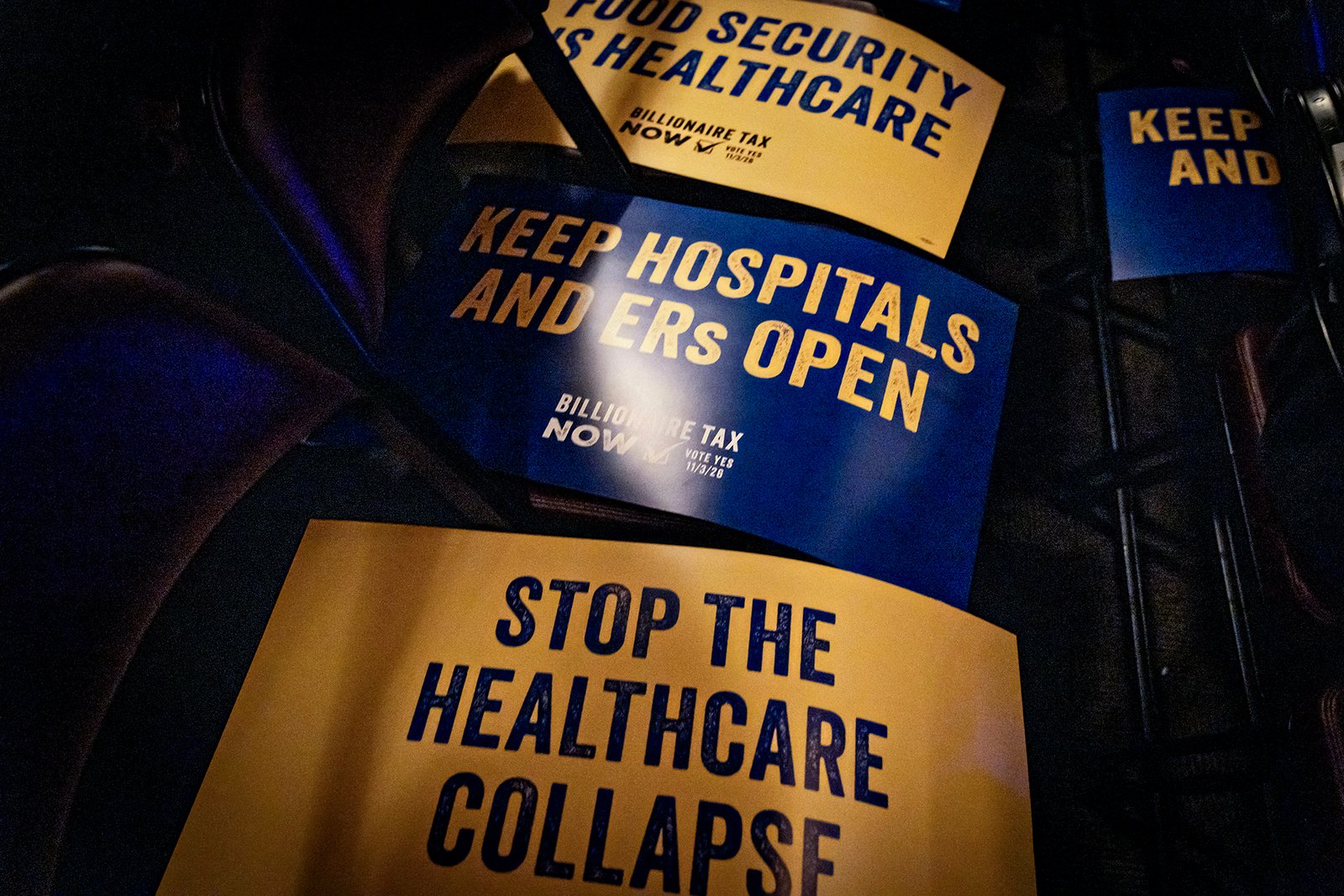

A popular proposal in California to impose a wealth tax on billionaires has gained enough signatures to qualify for the ballot in November, state officials announced on Wednesday.

The news is set to intensify an already heated debate around the tax, which has pitted tech moguls and the state’s governor, Gavin Newsom, against the labor union backing the measure.

The California Billionaire Tax Act, colloquially known as the billionaire tax, would levy a one-time 5% tax on any California resident worth more than $1bn. The proposal is backed by the Service Employees International Union-United Healthcare Workers West (SEIU-UHW) as a means of funding California’s strained healthcare, food assistance and education programs.

The proposal has become one of the state’s biggest political flashpoints. As it gained popular momentum throughout the year, it’s also prompted prominent billionaires, such as Google co-founder Larry Page and Meta co-founder Mark Zuckerberg, to makemoves to cut ties with the state and Newsom vowing to block it from going to a vote. Although it has gained enough signatures for the ballot, the coalition backing the measure has until 25 June to decide whether to move forward or potentially strike a deal.

While the union that floated the proposal has framed it as a way of getting the ultra-rich to pay their fair share, many of the state’s tech elites have condemned the tax and spent millions attempting to crush it. Google co-founder Sergey Brin has spent at least $82m alone on efforts to fight the tax and has relocated just over the California border to the Nevada side of Lake Tahoe.

The Palantir co-founder Peter Thiel, former Google CEO Eric Schmidt, crypto billionaire Chris Larsen and the DoorDash CEO, Tony Xu, are among other tech moguls who have donated millions to oppose the tax. California has the most billionaires out of any state – more than 200 – many of whom have increased their wealth in recent years amid the AI boom.

Notably, Jensen Huang, the billionaire CEO of Nvidia, has said he’s fine with the proposed tax and that he chose to live in Silicon Valley. During a talk at the Stanford Graduate School of Business in April, he said: “I say to everybody: ‘Move to California. Don’t leave.’ It’s the highest taxes in the world, but it’s OK.”

Battle lines

The proposed billionaire tax began to gain steam at the beginning of the year as the campaign sought to gather enough signatures to make it on to the November ballot. By late April, the SEIU-UHW said it had already filed more than 1.55m signatures – more than double the necessary amount and something the union has pointed to as testament to the popularity of the proposal.

On Thursday, the union announced it can now officially advance toward the November ballot.

“With today’s news, David won the second round against Goliath, but healthcare workers and our allies won’t quit until we protect patients from the looming California healthcare collapse manufactured by Trump and Congress,” said Debru Carthan, a spokesperson for the Billionaire Tax Now coalition.

The next step is for California’s secretary of state to confirm the measure by the 25 June deadline, which would officially certify it for November. The SEIU-UHW has the option, however, to withdraw it before next week. And this is where Newsom is stepping in.

The tech-friendly governor has long vowed to fight the measure. His spokesperson told the Guardian in January that he had consistently opposed such state-level wealth taxes, saying they “drive a race to the bottom”. He has publicly said that the tax would chase billionaires out of California and strip the state of revenue. Newsom is now reportedly whipping together a coalition to help him negotiate a deal with the union.

“From the get-go, SEIU-UHW has designed this measure as a ‘gun-behind-the-door’ to negotiate a better deal,” said David McCuan, a political science professor at Sonoma State University who studies the California ballot measure process. “Rather than go to the ballot and go nuclear in a ballot measure battle that can cost hundreds of millions of dollars, the goal has been to threaten to go to war.”

While several local unions and lawmakers, including the California congressman Ro Khanna, have joined the coalition to support the billionaire tax, powerful organizations in the state have also stepped in to oppose it. Those include the California Teachers Association, the State Building and Construction Trades Council of California, the California Medical Association and Planned Parenthood Affiliates of California.

McCuan said that made this week of capitol negotiations pivotal, adding that this was not the first time Newsom has waded into ballot measure campaigns. In 2024, the governor helped stave off several high-profile measures that had qualified for the November vote, including on issues such employer liability, children’s healthcare and oil drilling.

“Let’s see if that magic can be pulled off this time,” McCuan said, cautioning that the political climate was different this year with November shaping up to be the “mother of all midterms”.

“The stakes are much higher this time out,” he said.

The governor’s office declined to comment.

Food

Gas prices fall below $4 on average after Trump’s signing of Iran deal to end war

The average price of US gasoline fell to just under $4 a gallon on Thursday for the first time since March, following the announcement of a preliminary agreement between the US and Iran to end the war and reopen the strait of Hormuz.

The development has provided some relief to drivers who have seen soaring costs amid Washington’s war with Iran. But filling up still remains more expensive than it was before the conflict began.

According to the motor club AAA, the current national average price for a gallon of regular gasoline stands at $3.999, marking the first time in months that prices have been that low. The decline aligns with easing crude oil costs overall, with some optimism surrounding the initial agreement between the US and Iran.

Still, American drivers are collectively paying roughly $1 more per gallon than they were before the US joined Israel to attack Iran in February. Gas prices are also about 25% higher than they were a year ago, which has put strain on many household budgets across the country.

Gas isn’t the only thing that has become more expensive over the course of the war. Higher gasoline prices have also contributed to rising airline fares, while consumer goods such as groceries, and shoes have also gone up in cost amid global supply chain disruptions.

Even if oil and other core necessities – such as fertilizer – begin flowing from the Middle East again, experts warn that the sticker shock is likely to outlast the fighting.

“Product prices across the United States are projected to keep climbing for the rest of 2026,” Patrick Penfield, a professor of supply chain practice at Syracuse University, told the Associated Press on Thursday.

Penfield pointed to depleted inventories and ongoing supply chain consequences spanning from the war. He noted that farmers, for example, already had to pay higher costs for fertilizer and other supplies in the spring, which will “ripple through to increased food prices by autumn”. And at the gas pump, he noted that limited refinery capacity in the US “remains a significant bottleneck” towards bringing down prices.

The rising fuel costs have already pushed US inflation to its highest level in three years. And many consumers are still filling their tanks for much more than $4 a gallon.

That price is a national average, with costs varying between states due to factors such as proximity to supply and differing tax rates. In California on Thursday, regular gasoline averaged about $5.64 a gallon, according to AAA, followed by $5.57 in Hawaii. By contrast, prices in Indiana and Texas sat at about $3.40 and $3.49 a gallon.

Recent relief for fuel prices arrived with cooling costs for crude oil – the main ingredient in gasoline. Brent crude, the international standard, fell below $78 a barrel on Thursday, while US benchmark crude dropped to just over $74 a barrel. That’s still a little higher than the pre-Iran war level of roughly $70, but way below the $100-plus price seen a few weeks ago.

Major shipowners have reportedly begun moving vessels through the strait of Hormuz after Wednesday’s signing of the memorandum of understanding, according to maritime data from Lloyd’s List Intelligence – though some operators reported that only more limited side shipping routes were open.

On Thursday, US Central Command said in a statement that it has lifted its blockade on all maritime traffic entering and exiting Iranian ports and coastal areas in the strait of Hormuz.

“American forces are not impeding the transit of vessels to or from Iranian ports on the Arabian Gulf and Gulf of Oman,” it said.

Despite these developments, experts warn that it could take weeks or months for traffic to return to prewar levels.

The Associated Press contributed reporting

Food

Warsh shocks Wall Street with hawkish turn as Fed rate hikes come back into play

Federal Reserve Chair Kevin Warsh shocked Wall Street this week by delivering one of the most hawkish messages investors have heard in months, prompting traders to rapidly abandon expectations for interest-rate cuts and begin pricing in the possibility of rate hikes before year-end.

The dramatic shift in market sentiment came after the Federal Open Market Committee left rates unchanged but signaled that inflation remains its top concern despite signs of slowing economic growth.

The message was reinforced by former Dallas Fed President Robert Kaplan, who warned that policymakers may need to raise rates as soon as September if inflation fails to cool over the summer.

“If inflation prints don’t cool between now and we get to September, I actually think the balance of risks suggests it would be wise to take some action, either in September or in the fall,” Kaplan, now vice chairman at Goldman Sachs, said in an interview with Bloomberg Television.

Kaplan added that rate increases rarely come alone.

“If you move in September, you need to be prepared. There could be one or two more,” he said.

The hawkish turn caught many investors off guard. Earlier this year, markets largely expected the Fed’s next move to be a rate cut as economic growth moderated and inflation appeared to be moving closer to the central bank’s target.

Instead, Warsh’s debut as Fed chairman has shifted the conversation back toward inflation and the possibility that monetary policy may need to become even tighter.

“The odds of a rate hike are certainly higher than they were a month ago,” Scott Martin, partner at Kingsview Wealth Management, told The Post.

“The Fed has made it clear that inflation remains its primary concern, and if the next few inflation reports fail to show meaningful improvement, September is absolutely in play.”

Martin said the central bank appears increasingly focused on preserving its inflation-fighting credibility.

“Right now, it’s less about economic growth and more about protecting the Fed’s credibility on inflation,” he said.

Others see the Fed’s shift as even more dramatic.

Derek Reisfield, co-founder and former chairman of MarketWatch, said investors should prepare for higher borrowing costs.

“While the Fed rate remained unchanged for the moment, it is clear the positioning changed to reflect the increased likelihood of a rate hike later this year,” Reisfield said.

“I would say there is an 80 percent chance of a rate hike this Fall.”

Reisfield pointed to persistent inflation risks ranging from food prices to energy markets, warning that geopolitical uncertainty could keep inflation elevated through the end of the year.

The implications would extend far beyond Wall Street.

“Credit card, auto loan and other rates are likely to go up as well. So consumers will be paying more for credit all around,” Reisfield said.

Higher rates would also increase borrowing costs for the federal government as it finances its massive debt load.

For now, investors are left reassessing assumptions that had dominated markets for much of the year.

“I don’t think the market is overreacting,” Martin said.

“Investors spent much of the last year assuming the next move from the Fed would be a rate cut. Warsh is signaling that inflation is still a problem and that policymakers are willing to keep all options on the table.”

Food

California billionaire tax proposal qualifies for the November ballot

A proposal to raise taxes on the wealthiest Californians has qualified for the November ballot, state officials said Wednesday, setting up what could be an expensive and divisive fight.

The so-called billionaire tax — which has divided Democrats in the state — would implement a one-time tax on rich Californians if approved by voters.

California Secretary of State Shirley Weber said in a statement late Wednesday that the measure was eligible for the ballot this fall after her department verified the required number of signatures submitted by organizers.

There is still a chance, however, that the initiative will not appear on California’s ballot. The proposal’s supporters — led by Service Employees International Union-United Healthcare Workers West, a large California healthcare workers union — have until June 25 to decide whether they want to move forward with their push.

Several groups and lawmakers have for months engaged in negotiations over ways to reach a deal that would appease the unions supporting the tax while also preventing it from appearing on the ballot.

The measure has split prominent Democrats across the state.

Opponents have argued the initiative would drive wealthy investors and tech leaders from the state. California Gov. Gavin Newsom, widely seen as a presidential hopeful, has lined up in opposition to the billionaire tax.

Former Health Secretary Xavier Becerra, the leading candidate to succeed Newsom as governor, also opposes the tax.

On the other side, Rep. Ro Khanna, who also has his eye on a future White House bid, and Tom Steyer, a billionaire activist who ran unsuccessfully for governor, have backed the effort, arguing that it would help close income inequality gaps. Proponents have also made the case that it will help make up for state budget shortfalls as a result of Medicaid cuts in the “big, beautiful bill” that President Donald Trump signed into law last year.

The initiative would implement a one-time 5% tax on the assets of Californians whose net worth exceeds $1.1 billion. It would require the state to spend 90% of the new revenue on healthcare, with the remaining 10% split between education and food assistance programs. That discrepancy angered a number of Democratic groups advocating for education and food assistance.

In addition to the one-time tax on those worth more than $1.1 billion, it would implement a smaller tax on individuals worth between $1 billion and $1.1 billion. The taxes would apply retroactively to anyone living in the state as of Jan. 1, 2026.

Food

California billionaire tax qualifies for November ballot

A union wants California’s billionaires to rescue the state’s healthcare system. The billionaires have other ideas.

On June 17, an initiative to tax the state’s wealthiest residents qualified for the ballot, according to the secretary of state’s office, which verifies petition signatures.

Gov. Gavin Newsom, who has consistently swatted down the idea of tax increases throughout his tenure, emerged early as an opponent of the proposed tax. Wealthy allies in Silicon Valley joined the fray armed with deep pockets and threats to leave the state, which depends disproportionately on high earners for revenue.

The union funding the measure, Service Employees International Union-United Healthcare Workers West, says California needs the revenue that would be generated by the measure to rescue the healthcare system from deep cuts that the Trump administration made last year in the president’s tax reform package, known as the “One Big Beautiful Bill Act.”

Newsom is reportedly trying to negotiate a last-minute deal that would pull the initiative before the ballot is finalized on June 25.

What would it do?

The proposed initiative would levy a one-time 5% tax on California residents whose net worth exceeded $1 billion at the start of this year. The tax would hit roughly 200 people, and billionaires could pay in installments over five years.

Proponents of the measure estimate it would generate $100 billion for the state. The revenue would go into a special fund with 90% reserved for healthcare spending and 10% for education and food assistance programs.

The Legislature would control the funds and could allocate up to $25 billion annually to designated programs including Medi-Cal and CalFresh.

It needs a simple majority to pass.

Who is supporting it?

The state’s largest healthcare workers union is bankrolling the measure, pouring more than $31 million into the campaign. “We are facing literally a collapse of our healthcare system here in California and elsewhere,” Dave Regan, president of SEIU-UHW, said in October when the campaign launched.

The union, which is known for wielding ballot measures aggressively, argues that federal healthcare cuts will result in hospital and clinic closures, worsened patient access and thousands of lost jobs if the state doesn’t step in to backfill tens of billions of federal dollars. The group also points out that the Trump tax breaks for income, businesses and investments disproportionately benefit the wealthy people who would then be subject to the proposed billionaire tax.

“Whether or not folks support this, they can’t deny that these massive cuts to healthcare are coming,” said union spokesperson Renée Saldaña. “Nobody else has a solution to fill this massive $100 billion funding gap that is facing California.”

Saldaña noted that people signing the initiative petition were supportive and sometimes wanted the tax to be continuous rather than one-time.

“This is popular. The public is feeling the strain of their own healthcare costs,” she said.

The measure has won high-profile support from Vermont Sen. Bernie Sanders and former Secretary of Labor Robert Reich. A handful of local unions as well as the Teamsters and AFSCME California have also backed the measure.

Who is opposed to it?

Newsom is an unsurprising and vocal critic of the proposal. He has long argued that increased taxes would drive wealthy people and businesses out of the state. In a recent appearance on Real Time with Bill Maher, Newsom claimed that “we’ve already seen dozens and dozens of people leave the state.”

Google co-founder Sergey Brin, with a net worth of $300 billion, according to Forbes, reportedly moved to Nevada because of the tax threat. Brin, a one-time supporter of liberal causes turned Trump supporter, is also the biggest spender among opponents. As of June 15, he has contributed $82 million to Building a Better California, which is funding multiple countermeasures designed to invalidate or weaken the initiative should it pass. The committee has not, however, taken a position on the wealth tax.

The top two measures — the Retirement and Personal Savings Protection Act and the Improving Transparency, Effectiveness and Efficiency in California Government Act — will also likely appear on the November ballot. The retirement act would prohibit new state taxes on personal property, effectively canceling the billionaire tax if both measures pass. The transparency act would require audits of state programs funded by special taxes.

Other tech and industry titans, including Google CEO Eric Schmidt, worth $43.3 billion, Kleiner Perkins chairman John Doerr, worth $25 billion, and The Wonderful Company president Stewart Resnick, worth $5.4 billion, have donated millions of dollars to Brin’s committee.

Ripple Labs co-founder Chris Larsen, worth an estimated $12.4 billion, also started Golden State Promise, a political action committee dedicated to opposing the tax initiative directly. Venture capitalist Ron Conway, who does not appear on Forbes’ billionaires list, is funding a third group, Stop The Squeeze.

Collectively, the opposition campaigns have raised $107.9 million as of June 15, according to state campaign finance data.

Robert Lapsley, president of the California Business Roundtable, said one of the most concerning parts of the proposal is a provision allowing the Legislature to amend the tax after passage. “They can change the level of taxation; they can change how often they get taxed; they can keep ratcheting down the income level of who pays it.” The union disputes this claim.

Progressive groups like Planned Parenthood and the California Teachers Association have opposed the measure in recent weeks. Healthcare industry groups like the California Medical Association, California Primary Care Association and California Hospital Association also oppose it.

What’s really going on with healthcare?

The “One Big Beautiful Bill Act,” which Congress passed last year, enacts a number of sweeping changes to Medicaid, the health insurance program for low-income people and those with disabilities.

Over time, experts say the changes will dramatically reduce the number of people with publicly funded insurance through mandates such as work requirements and shorter eligibility periods. The law also limits federal Medicaid spending. Because Medicaid programs draw on state and federal dollars, reductions in enrollment or federal spending mean less money for states like California.

The state Department of Health Care Services projected early on that federal cuts could cost California $30 billion annually. Roughly 14 million people rely on Medicaid, also known as Medi-Cal, in California.

State lawmakers have also grappled with successive budget deficits and ballooning program costs. Last year, Newsom and the Legislature limited Medi-Cal enrollment for low-income people without legal status. State leaders are eyeing additional cuts this year to align with new federal requirements.

Miranda Dietz, director of the Health Care Program at the UC Berkeley Labor Center, said close to 3 million Californians will lose healthcare over the next two years as a result of state and federal changes.

“The need for health insurance and healthcare is not going anywhere,” Dietz said.

What are the challenges?

Should the measure pass, it will surely face legal challenges that could tie the potential revenue up for years, experts say. The seemingly retroactive nature of the tax invites a constitutional challenge, many say, though supporters reject those concerns. The initiative proposes taxing those who are California residents as of Jan. 1, 2026, meaning those who have since left the state would still owe it.

Mark Peterson, a public policy professor at UCLA School of Law, said revenue from the initiative would “make a huge difference” in helping the state offset federal funding losses, but that’s only if the initiative survives legal challenges and efforts by billionaires to move or hide assets.

Economists and state budget watchers are also wary of the number of billionaires who have already left the state, taking their assets and businesses with them. Only six people moved out of state last year before the proposed tax would apply to them, but their collective worth would have generated the state $27 billion, Fortune reported. Others, including Meta CEO Mark Zuckerberg, worth $231 billion, have also reportedly moved out but not before Jan. 1.

On the other hand, there’s no evidence yet that a majority of the state’s 200 billionaires are leaving. Some, including former gubernatorial candidate and billionaire Tom Steyer, have stated they support the proposal.

Early polling shows 50% of voters favor the initiative, with most strongly behind it, according to the UC Berkeley Citrin Center for Public Opinion Research-POLITICO poll. But that is not as strong a position as it may seem: 54% of voters are concerned about wealthy individuals leaving the state, and 63% are concerned about them taking their businesses with them. A UC Berkeley Institute of Government Studies-Los Angeles Times poll from March showed similar division among voters with 52% in support.

Generally, campaigns running ballot initiatives want their early polling numbers to be much higher because support nearly always dwindles as the election creeps closer.

Supported by the California Health Care Foundation (CHCF), which works to ensure that people have access to the care they need, when they need it, at a price they can afford. Visit www.chcf.org to learn more.

Food

Lincoln Memorial Reflecting Pool before and after

Algae returns to the Lincoln Memorial Reflecting Pool days after the Trump administration’s $14.2 million overhaul.

Days after the completion of the Lincoln Memorial Reflecting Pool’s renovations, the “American flag blue” pool turned green because of algae. The Trump administration spent $14.2 million on a no-bid contract to have the bottom of the reflecting pool painted and the seams resealed in preparation for the country’s 250th birthday this summer. The algae were visible from the water’s edge a day after the reservoir was filled and workers could be seen clearing algae from the bottom of the pool last week.An Interior Department spokesperson told CNN the algae is residual and a normal part of the early process of restarting operations at the reflecting pool. “What you are seeing is residual algae from the supply lines, which have been sitting dormant for eight weeks while construction has been taking place. It’s part of the normal startup process. We are removing the algae, and the nanobubblers will maintain the pool and keep it algae free,” communications director Kate Martin said in a statement.Scroll below for a photo timeline of the reflecting pool’s renovation.What causes algae bloom?Algae are plant-like organisms that use sunlight, water and carbon dioxide to create their own food. These organisms thrive in places with warm water temperatures, abundant sunlight and stagnant water.The reflecting pool, which is more than 2,000 feet long, was originally built in the 1920s. Its shallow, slow-moving water has long been prone to appearing green in the summer, particularly when heat, sunlight and stagnant conditions combine.

Days after the completion of the Lincoln Memorial Reflecting Pool’s renovations, the “American flag blue” pool turned green because of algae.

The Trump administration spent $14.2 million on a no-bid contract to have the bottom of the reflecting pool painted and the seams resealed in preparation for the country’s 250th birthday this summer.

Advertisement

The algae were visible from the water’s edge a day after the reservoir was filled and workers could be seen clearing algae from the bottom of the pool last week.

An Interior Department spokesperson told CNN the algae is residual and a normal part of the early process of restarting operations at the reflecting pool.

“What you are seeing is residual algae from the supply lines, which have been sitting dormant for eight weeks while construction has been taking place. It’s part of the normal startup process. We are removing the algae, and the nanobubblers will maintain the pool and keep it algae free,” communications director Kate Martin said in a statement.

Scroll below for a photo timeline of the reflecting pool’s renovation.

What causes algae bloom?

Algae are plant-like organisms that use sunlight, water and carbon dioxide to create their own food. These organisms thrive in places with warm water temperatures, abundant sunlight and stagnant water.

The reflecting pool, which is more than 2,000 feet long, was originally built in the 1920s. Its shallow, slow-moving water has long been prone to appearing green in the summer, particularly when heat, sunlight and stagnant conditions combine.

If Trump's Iran deal is good for the US, why the GOP outrage?

Months of war and a blockade have battered Iran. Its navy is at the bottom of the Persian Gulf. Its...

Grammy-nominated producer Tay Keith found dead in Nashville apartment, police confirm

NASHVILLE, Tenn. (WSMV) – Metro Nashville Police have confirmed the death of Grammy-nominated producer Brytavious Chambers, better known as Tay...

US lifts naval blockade as Iran supreme leader says Trump made deal 'out of desperation' | BBC News

The US has confirmed it has lifted its naval blockade of Iranian ports, as the Iran deal comes into effect....

Obama's open presidential centre in Chicago. #BBCNews

Canada v Qatar: World Cup 2026 – live

Key events “There’s no point in beating a dead horse,” says Rebekah Voss, gawping at a dead horse, “but I...

Waymo recalls robotaxi fleet after construction-zone freeway incidents

Waymo is recalling nearly 4,000 robotaxis after more than a dozen incidents in which the autonomous vehicles entered closed freeway...

NYC celebrates Knicks championship win for first time in over 50 years. #BBCNews

‘All My Children’ star Paul Avery and wife killed in house fire

“All my Children” star Paul Avery and his wife, Sheila, tragically died in a devastating house fire in the early...

US-Iran deal triggers 60-day period to reach final agreement | BBC News

The US and Iran have signed a 14-point Memorandum of Understanding, triggering a 60-day period to reach a final agreement.

Obama: Some presidential center exhibits reflect 'unfinished business'

At the opening of his presidential center, former President Barack Obama said some exhibits reflect the “unfinished business” of …

-

Business5 days ago

Business5 days agoHow much of Musk’s wealth comes from government help? Virtually all of it

-

LifestyleNews2 weeks ago

LifestyleNews2 weeks ago120 minutes of strength training per week may help extend lifespan

-

Politics1 week ago

Politics1 week agoWhat to know about the stabbing that set off fiery riots in Northern Ireland

-

Video6 days ago

Video6 days agoDownload fans say what they love about the festival. #DownloadFestival #BBCNews

-

Video6 days ago

Video6 days agoWhy SpaceX IPO isn't about space. #SpaceX #ElonMusk #BBCNews

-

HealthNews7 days ago

HealthNews7 days agoThe people of Okinawa, Japan only eat until they are about 80 percent full, then stop — and the practice has been linked in multiple peer-reviewed studies to lower rates of cardiovascular disease, slo

-

TravelNews6 days ago

TravelNews6 days agoMy Paternal Instinct Should’ve Warned Me About Netflix’s Maternal Instinct

-

Food6 days ago

Food6 days agoPope Leo’s plane was grounded. Then the King of Spain stepped in to help